As the financial landscape evolves, understanding generational differences in banking behaviors is more critical than ever. This article explores the banking behaviors and preferences of Gen Z, Millennials, and Gen X, and provides insight into how these generations are influencing the financial future of their children (Gen A), now aged 8-18 years old. By 2025, Gen A is projected to become the largest generation, with a population reaching 2 billion and a spending power anticipated to surpass that of any previous generation.

The behaviors of Gen Z and Millennials, offer a preview of the banking demands that Gen A will bring. Both groups are already driving a shift toward digital convenience and fee transparency in their own banking choices.

Gen X, while less digitally focused, provides a bridge between traditional banking practices and the digital expectations of younger generations. Together, these generational dynamics point toward a future where financial institutions must adapt rapidly to serve a new generation raised with digital-native values and expectations.

The findings are based on data collected from a Woli survey of men and women aged 18 to 59 years old, exploring the generational preferences and behaviors that drive banking choices today. As banking continues to shift toward digital platforms, understanding these differences is critical for banks seeking to cultivate long-term, meaningful relationships with customers of all ages.

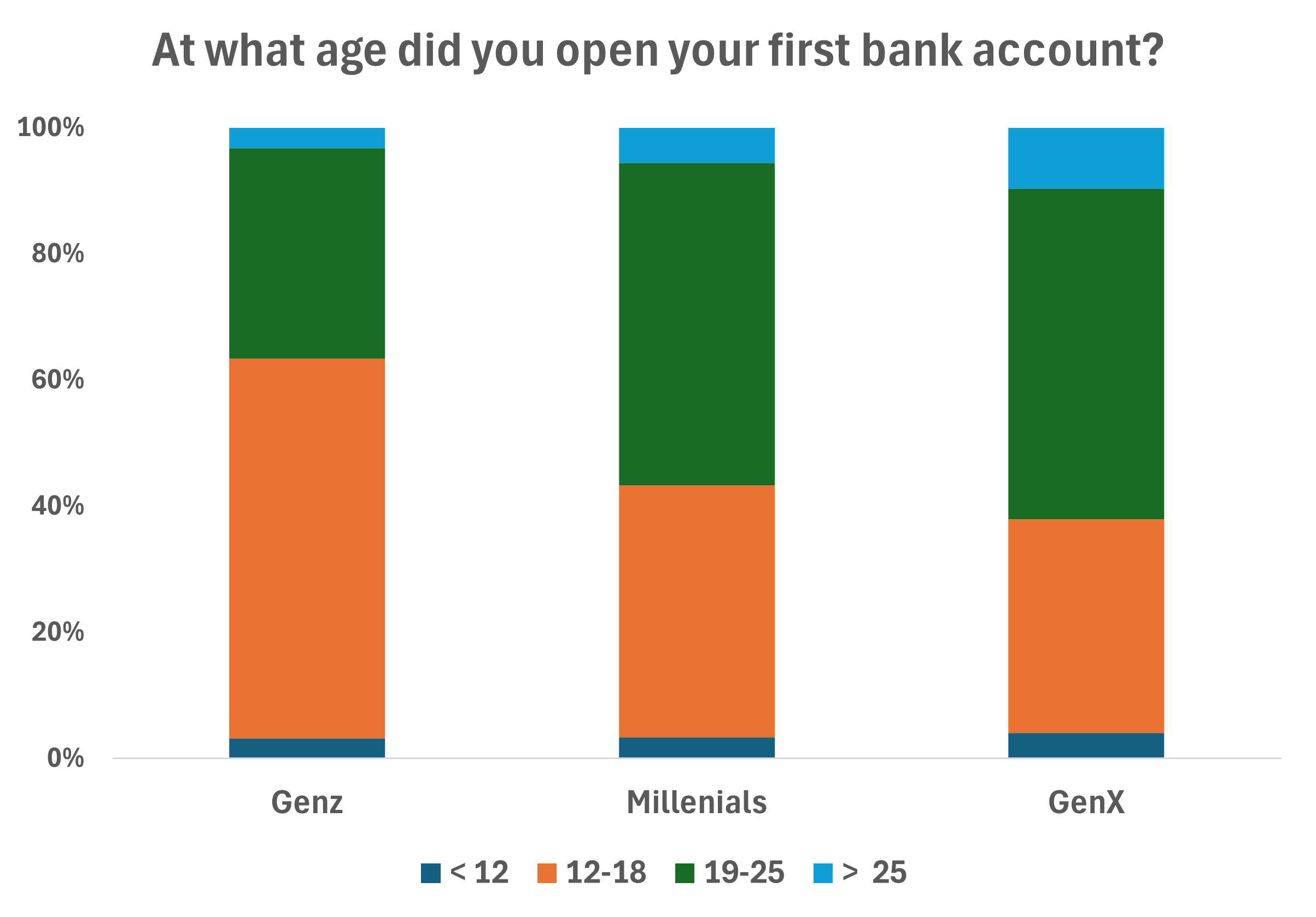

Understanding the Age of First Banking Experience

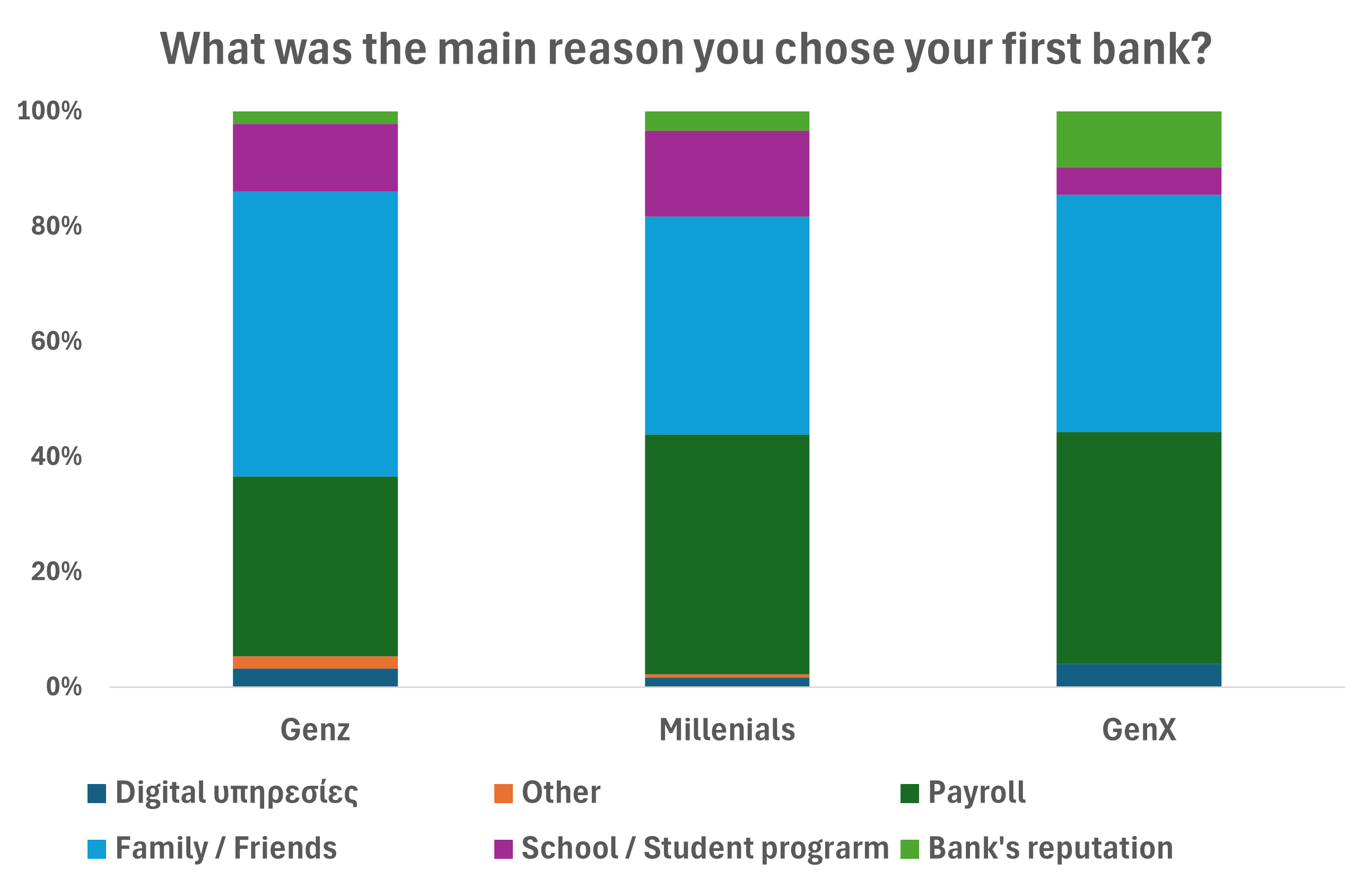

Gen Z (aged 12-27) is the first generation that tends to open a bank account before they reach adulthood (between 12-18), often influenced by parents or friends who try to introduce financial responsibility early on.

Millennials (aged 28-43): Generally opened their first accounts around age 19-25, mainly for business reasons (payroll account).

Similar to Millennials, Gex X (aged 44-59) opened their first bank account between the ages of 19-25. Influence by family or friends as well as business reasons (payroll account) are the main reasons for choosing their first bank.

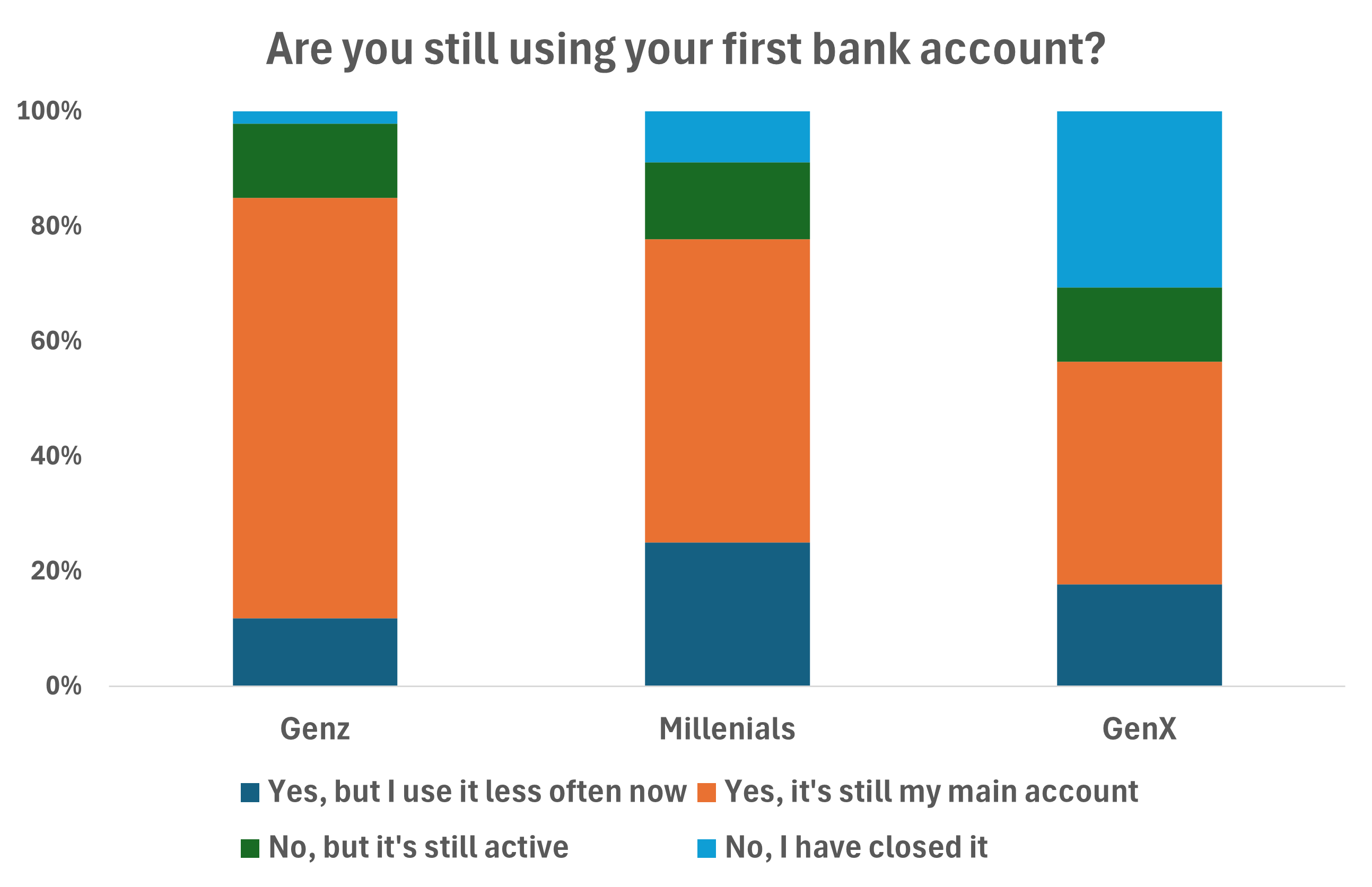

Loyalty to the First Bank Account

As expected given their young age, the majority of Gen Z still use their first bank account as their main.

Similarly, 91% of Millennials still use their first bank account, although 38% of them say it’s not their primary one.

30% of Gen X have closed their first accounts, often seeking better terms elsewhere.

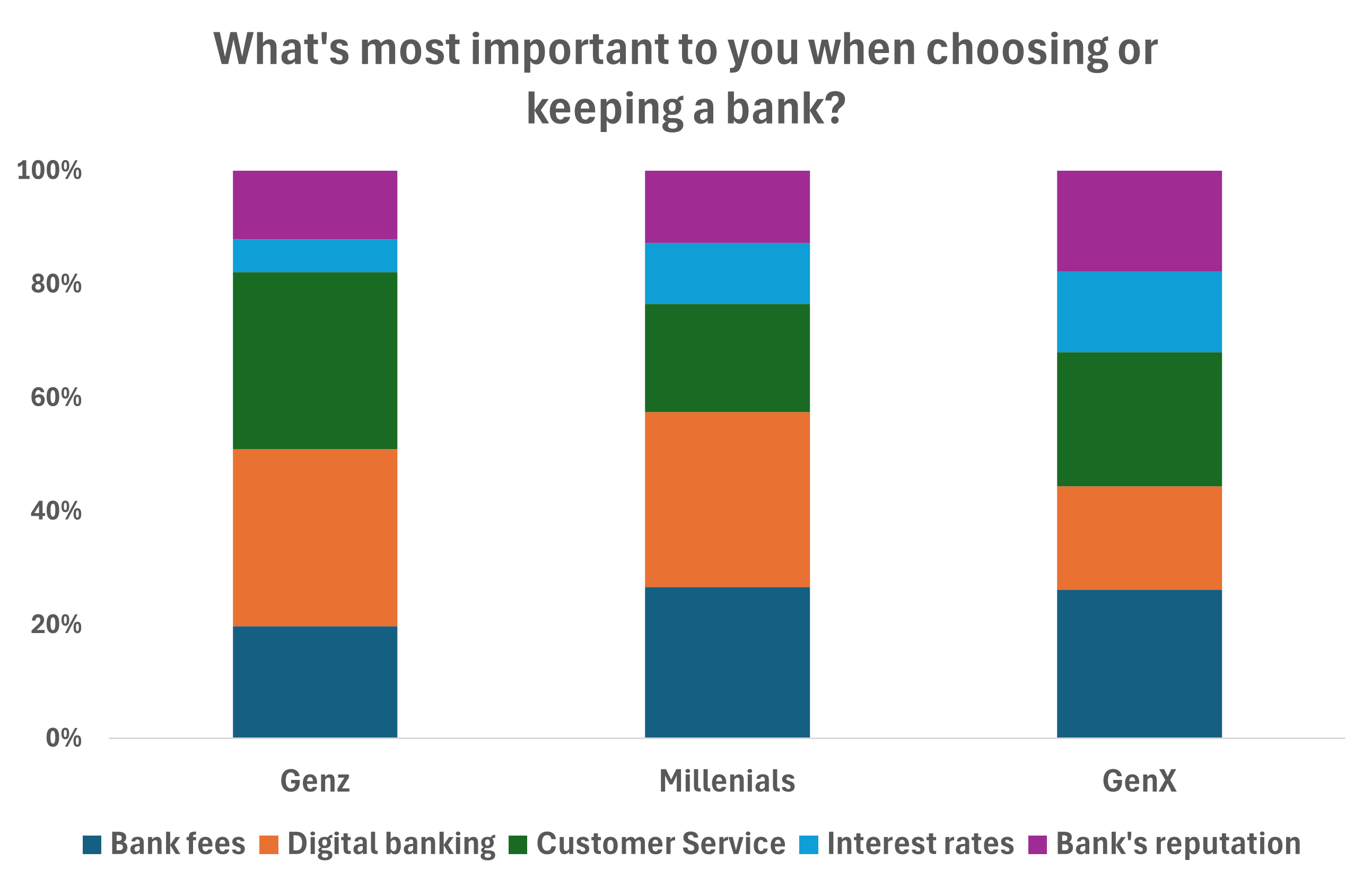

Reasons for Choosing a Bank

Gen Z tends to place a strong emphasis on the overall banking experience (over 60%), with a particular focus on digital capabilities and reliable customer support.

Digital capabilities (31%) are also important for Millennials, which equally values fee rates.

Gen X tends to choose banks based on fee rates (26%) and customer support (24%) They consider digital capabilities and brand reputation as equal factors (18%).

Conclusion

As banking preferences evolve across generations, financial institutions face both opportunities and challenges in adapting to these shifts. Gen Z and Millennials, known for their affinity for digital convenience and fee transparency, have set a new standard in banking expectations, one that prioritizes user-friendly technology and accessible financial products. Gen X, although less digitally driven, values a balance between digital features and quality customer service, reflecting a blend of traditional and modern banking needs.

With Gen A on the horizon, the influence of their Gen Z and Millennial parents is already shaping future banking demands. Financial institutions must prioritize innovation, focusing on digital capabilities and transparent pricing to align with the digital-native values of upcoming generations. By understanding these generational differences, banks can build long-lasting relationships and remain relevant in a rapidly transforming financial landscape.